Why Sonas Is Flat-Fee

We choose to offer our services under a flat-fee fee-only business model in order to minimize any conflicts of interest which can compromise the advice you receive from us. We pride ourselves on transparency and offering advice in our clients’ best interest. We serve as a professional partner to help clients navigate important financial choices that impact their lives. With an intimate understanding of our clients, and specialized skills and resources, we help identify opportunities and coach actions/behaviors which can benefit them.

Our flat fee structure is based on a commitment to placing client interests first, providing transparent & predictable pricing, and making financial advisory services more accessible. Financial Review (aka “Try before you buy”) clients and full-service clients will receive a comprehensive financial review & retirement field guide to achieve their retirement goals.

Want to learn more? Set up some time to have a conversation to see if we might be a good fit for your needs and preferences.

Fee-Only. Fiduciary. Independent.

What does it all mean for you?

Fee Only - We only get paid by YOU. Complete transparency. No products, no commissions, no hidden charges… no conflicts of interest.

Fiduciary - We only do and advise what is in YOUR best interest. Not ours.

Independent - Results for YOU, not shareholders or private equity stakeholders. No sales quotas. No toeing the company line. We are not tied to any family of funds, investment products, or insurance products.

Flat-Fee - Working with a flat-fee financial advisor reduces conflicts of interest and allows more of your money to compound for you, not against you. We believe it’s unfair to pay more simply because you’re worth more. Our fixed-dollar fees reflect our work, not your net worth.

What is Flat-Fee,Fee-Only, & Fiduciary?

Compensation Structure for Financial Advisors

To truly understand the value of a fee-only advisor, it is important to understand the different ways advisors can get paid. The three most common methods include:

Commission-based

Fee-based

Fee-only

Commission-based representatives typically don’t charge fees to their clients. Instead, they earn commissions based on the insurance or investment solutions they recommend. Not surprisingly, the clients of commission-based financial representatives can find themselves owning products that pay commissions to the producer who sold them. Under this model, it’s hard for the client to really know whether the recommendations made for them were in their best interest, or simply earned their advisor strong commissions. The products the clients are put into can also lack transparency and be very difficult to get out of or change.

Fee-based advisors typically work for big investment companies. “Fee-based” is often confused with “fee-only,” but there are important distinctions. Fee-based advisors do charge clients a fee (typically a percent of assets under management), but they also can make commissions from financial products and transactions. They earn part of their revenue from selling products on behalf of brokerage firms, mutual fund companies, or insurance companies, thus placing them at the same risk for conflicts of interest as commission-based representatives.

Fee-only financial advisors are paid directly by their clients—and only by their clients. They don’t receive any type of incentive or commission for recommending certain securities or investments. Their fees are typically structured as a small percentage of the assets they manage, known as assets under management (AUM). Some fee-only advisors offer hourly planning services or amonthly or annual fixed fee for ongoing services as well. Because fee-only advisors only get paid by their clients, they avoid many of the conflicts of interest that can get in the way of clients receiving advice that is in the clients’ best interest.

The Benefits of Working With a Fee-Only Financial Advisor

The National Association of Personal Financial Advisors (NAPFA) believes fee-only advisors are the most transparent and unbiased advisors. (1) They typically have one of two titles: either registered investment advisor (RIA) or CERTIFIED FINANCIAL PLANNER™. If you are in the market for a financial advisor, here are two reasons you should choose a fee-only advisor:

1. Reduced Conflicts of Interest

No matter how pure an advisor’s intentions are, it can be difficult to provide unbiased advice if they have a financial incentive to recommend action steps, products, or services that will increase revenue and profits. Fee-only advisors have no financial incentive to push one product over another, thus avoiding a common conflict of interest.

2. Fiduciary Commitment

Fee-only advisors are fiduciaries, which means they are legally and ethically obligated to act in their clients’ best interest at all times and to disclose any potential conflicts of interest. If you’re their client, they are loyal to you and provide objective financial advice based on your unique situation and goals.

Flat-Fee

The flat-fee model is a modern pricing structure that challenges the status quo of asset-based pricing and commissioned sales.

Price is determined by the service provided, rather than the portfolio size or products sold. Advisors are free to give unbiased advice without compensation incentives tilting their recommendations. Thus, this model reduces client/advisor conflicts of interest.

Flat-fee firms typically offer various services – ongoing advice with optional investment management as well as limited engagements through project-based or hourly work.

Conflicts of Interest with Flat-Fee

It’s challenging to imagine conflicts of interest that are unique to this pricing model. However, you could point to conflicts in any business transaction- the buyer wants to pay less, and the seller wants to charge more.

Similarly, firms that offer hourly work could be incentivized to overstate their hours and collect more revenue. It is unlikely that either of these potential conflicts would bias the advice given to clients.

Other Issues with Flat-Fee

The flat-fee model can be more expensive than AUM early in an investor’s journey. For example, a family with $250,000 of assets would pay $2,500 for the first year under 1% AUM (if they meet the asset minimum). Similarly, a flat-fee planner could charge $4,000 – $6,000 for a year of service. It’s important to point out that AUM fees often only include investment management, whereas flat-fee service usually has a broader scope (including planning).

Additionally, flat-fee doesn’t mean “fixed-fee”. It’s reasonable to expect a firm to raise prices over time as the cost of living and business expenses rise. However, the fee increases will almost always pale in comparison to how quickly the AUM fees grow over time.

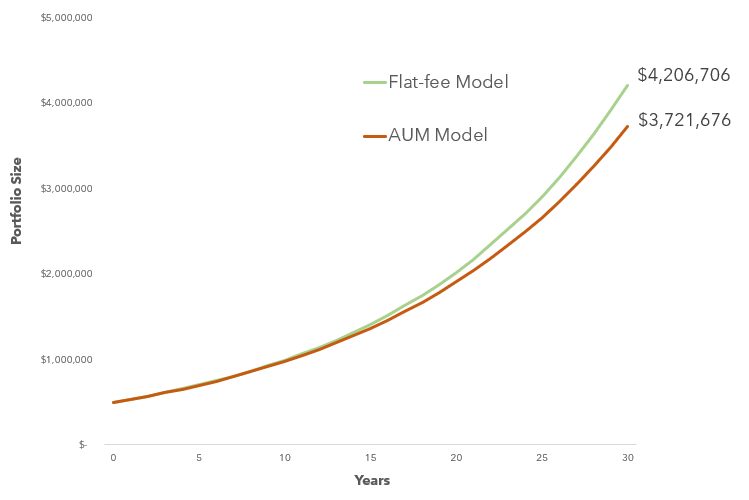

Below is a comparison of how a 1% AUM fee and a flat-fee impact a $500,000 portfolio over time. Both start at the same dollar value, but the AUM fee grows with the portfolio at 8% annually, whereas the flat-fee increases at the inflation rate (3%).

The difference in ending account value over 30 years is staggering – almost $500,000, which was the initial investment!

If you assume retirement at the end of the timeline using the 4% rule, the flat-fee investor would have $155,000 of annual pretax income after fees, and the AUM investor would receive $111,000 – a 28% decrease. A smaller retirement portfolio and a higher advisor fee through retirement explain the difference in income.

Conclusion

No fee model is perfect, but obviously some are better at protecting the client’s interests (and wealth) than others.

Considering the conflicts of interest and the issues described above, I think it wise investors narrow their search to only flat-fee advisors.

What do you think?